Featured

Table of Contents

Current Rates Of Interest Trends in Oklahoma City Debt Consolidation Without Loans Or Bankruptcy

Customer debt markets in 2026 have actually seen a considerable shift as charge card rate of interest reached record highs early in the year. Numerous residents across the United States are now facing interest rate (APRs) that go beyond 25 percent on standard unsecured accounts. This economic environment makes the expense of bring a balance much higher than in previous cycles, requiring individuals to look at financial obligation decrease techniques that focus specifically on interest mitigation. The two primary approaches for achieving this are financial obligation combination through structured programs and debt refinancing via new credit products.

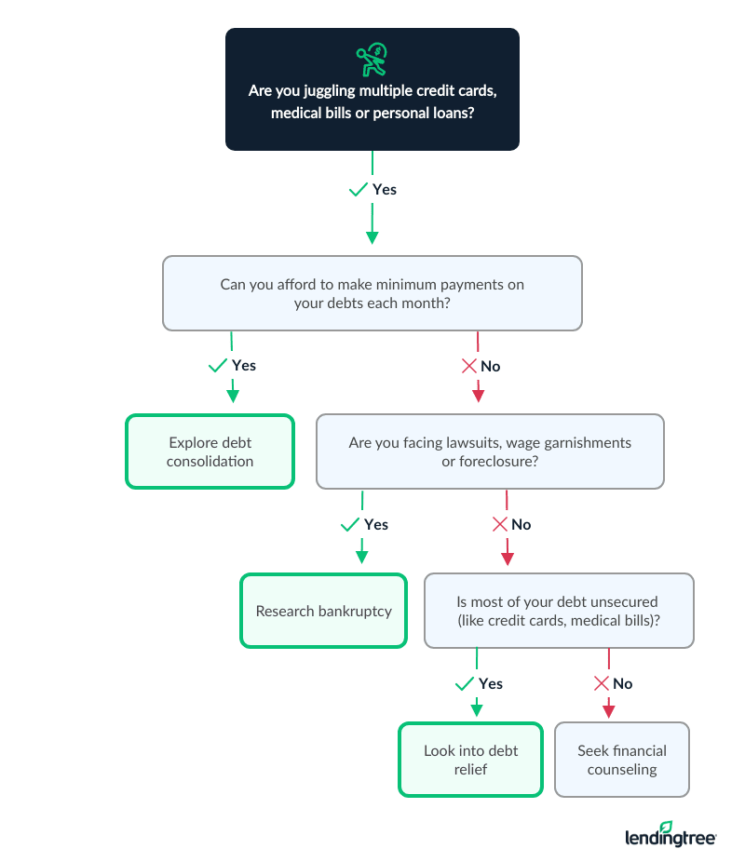

Managing high-interest balances in 2026 requires more than simply making bigger payments. When a substantial part of every dollar sent to a financial institution goes toward interest charges, the primary balance hardly moves. This cycle can last for years if the rate of interest is not lowered. Households in Oklahoma City Debt Consolidation Without Loans Or Bankruptcy typically find themselves choosing between a nonprofit-led financial obligation management program and a personal consolidation loan. Both alternatives objective to streamline payments, but they function in a different way relating to rate of interest, credit report, and long-term monetary health.

Lots of households understand the value of Certified Debt Management Programs when handling high-interest credit cards. Choosing the right path depends upon credit standing, the overall quantity of financial obligation, and the ability to keep a rigorous regular monthly spending plan.

Not-for-profit Debt Management Programs in 2026

Nonprofit credit therapy agencies use a structured technique called a Debt Management Program (DMP) These companies are 501(c)(3) organizations, and the most reputable ones are approved by the U.S. Department of Justice to supply specific therapy. A DMP does not involve securing a brand-new loan. Instead, the company negotiates straight with existing lenders to lower interest rates on existing accounts. In 2026, it prevails to see a DMP minimize a 28 percent credit card rate to a variety between 6 and 10 percent.

The process involves consolidating numerous monthly payments into one single payment made to the firm. The firm then distributes the funds to the various financial institutions. This method is available to homeowners in the surrounding region despite their credit report, as the program is based on the agency's existing relationships with national loan providers instead of a new credit pull. For those with credit rating that have already been affected by high financial obligation usage, this is typically the only viable method to secure a lower rates of interest.

Expert success in these programs often depends on Debt Management to guarantee all terms are beneficial for the customer. Beyond interest decrease, these companies likewise offer monetary literacy education and real estate therapy. Because these companies often partner with local nonprofits and community groups, they can provide geo-specific services customized to the requirements of Oklahoma City Debt Consolidation Without Loans Or Bankruptcy.

Refinancing Financial Obligation with Personal Loans

Refinancing is the procedure of getting a brand-new loan with a lower rates of interest to settle older, high-interest debts. In the 2026 lending market, personal loans for financial obligation consolidation are widely available for those with good to outstanding credit report. If a specific in your area has a credit history above 720, they might qualify for an individual loan with an APR of 11 or 12 percent. This is a substantial improvement over the 26 percent often seen on charge card, though it is generally greater than the rates negotiated through a not-for-profit DMP.

The primary advantage of refinancing is that it keeps the customer in complete control of their accounts. As soon as the individual loan settles the charge card, the cards remain open, which can help lower credit usage and possibly enhance a credit history. This presents a danger. If the individual continues to use the charge card after they have been "cleared" by the loan, they might wind up with both a loan payment and new charge card debt. This double-debt scenario is a common risk that financial therapists warn versus in 2026.

Comparing Total Interest Paid

The primary goal for many people in Oklahoma City Debt Consolidation Without Loans Or Bankruptcy is to decrease the total amount of money paid to lending institutions over time. To comprehend the distinction in between debt consolidation and refinancing, one must take a look at the overall interest cost over a five-year duration. On a $30,000 debt at 26 percent interest, the interest alone can cost countless dollars annually. A refinancing loan at 12 percent over five years will significantly cut those costs. A financial obligation management program at 8 percent will cut them even further.

Individuals often look for Debt Management in Oklahoma City OK when their monthly obligations surpass their income. The difference in between 12 percent and 8 percent might appear little, however on a large balance, it represents thousands of dollars in savings that remain in the customer's pocket. Moreover, DMPs typically see lenders waive late costs and over-limit charges as part of the settlement, which supplies instant relief to the total balance. Refinancing loans do not typically provide this advantage, as the new lender merely pays the existing balance as it stands on the declaration.

The Impact on Credit and Future Loaning

In 2026, credit reporting companies see these two methods in a different way. A personal loan utilized for refinancing appears as a new installment loan. At first, this might cause a little dip in a credit history due to the difficult credit inquiry, but as the loan is paid for, it can strengthen the credit profile. It demonstrates an ability to manage various types of credit beyond simply revolving accounts.

A debt management program through a nonprofit firm includes closing the accounts consisted of in the strategy. Closing old accounts can briefly lower a credit report by minimizing the typical age of credit rating. However, many participants see their ratings enhance over the life of the program due to the fact that their debt-to-income ratio enhances and they develop a long history of on-time payments. For those in the surrounding region who are thinking about bankruptcy, a DMP acts as a vital middle ground that prevents the long-term damage of an insolvency filing while still offering considerable interest relief.

Selecting the Right Course in 2026

Deciding in between these 2 alternatives needs a sincere evaluation of one's financial scenario. If a person has a steady earnings and a high credit score, a refinancing loan offers versatility and the possible to keep accounts open. It is a self-managed option for those who have currently fixed the costs practices that led to the financial obligation. The competitive loan market in Oklahoma City Debt Consolidation Without Loans Or Bankruptcy means there are many alternatives for high-credit borrowers to find terms that beat charge card APRs.

For those who require more structure or whose credit report do not permit low-interest bank loans, the not-for-profit financial obligation management route is often more reliable. These programs provide a clear end date for the financial obligation, typically within 36 to 60 months, and the negotiated rate of interest are often the most affordable readily available in the 2026 market. The inclusion of financial education and pre-discharge debtor education ensures that the underlying causes of the financial obligation are addressed, lowering the possibility of falling back into the very same scenario.

Despite the selected approach, the top priority stays the same: stopping the drain of high-interest charges. With the financial environment of 2026 providing distinct challenges, taking action to lower APRs is the most reliable way to guarantee long-lasting stability. By comparing the terms of personal loans against the advantages of nonprofit programs, homeowners in the United States can find a course that fits their particular spending plan and objectives.

{kind=link}

Latest Posts

Is Bankruptcy the Right Financial Path in 2026?

Mortgage and Debt Counseling for Families in 2026

Evaluating Debt Management Against Bankruptcy for 2026